Robo-advice and the cost of convenience

Thinking about using a robo-advisor? It could cost you.

Published: Wednesday, December 1st, 2021

Key points:

- Self-directed management remains a competitive alternative to robo-advice and traditional active management.

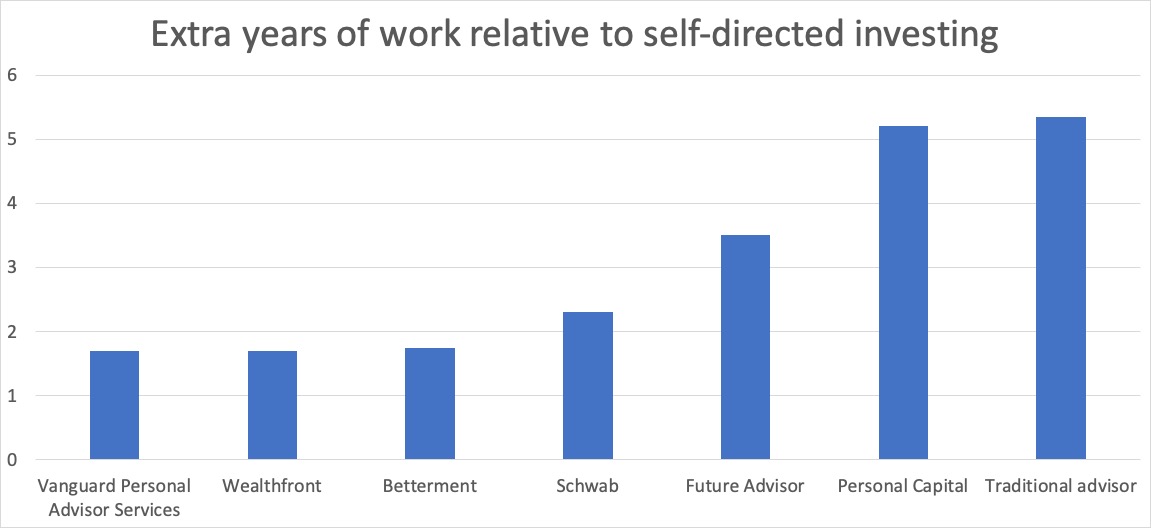

- Using a robo-advisor can delay retirement by 2-5 years compared to self-directed management.

- Robo-advisors will likely become more competitive in the future.

By the end of 2021, roughly 3.5 million adults were expected to delegate portfolio management to a robo-advisor. Outside of employer-sponsored plans, the appeal of automated investing is evident: fast account setup, risk‑tolerance questionnaires, and automatic rebalancing eliminate much of the friction that deters novice investors. When combined with data showing that over 90% of active fund managers have trailed the S&P 500, it is understandable why many are willing to entrust algorithms with their retirement savings.

Robo‑advisors have simplified the investment process to an admirable degree. A few clicks and recurring contributions are directed into a pre‑set portfolio, and some providers even perform automated tax‑loss harvesting to enhance after‑tax returns. The convenience is undeniable.

Self‑directed investing, by contrast, demands a more active participant. Investors must become familiar with concepts such as bid/ask spreads, market and limit orders, and the mechanics of portfolio rebalancing. Frequent access to account balances and asset prices can tempt some individuals to trade impulsively or to make costly errors. Even for those with steady nerves, the question remains: how should one value the time spent managing a portfolio versus delegating it to software?

This article quantifies the economic cost of that convenience by comparing typical robo‑advisor fees against a low‑cost, self‑directed passive strategy in 2021.

Quantifying the cost

Using Nesteggly’s Ultimate Retirement Calculator, we estimated the additional years of employment required to offset the aggregate fees charged by leading robo‑advisors relative to a self‑directed portfolio invested in broad market index funds. The result was striking: under reasonable return assumptions, reliance on a robo‑advisor would delay retirement by approximately two to five years.

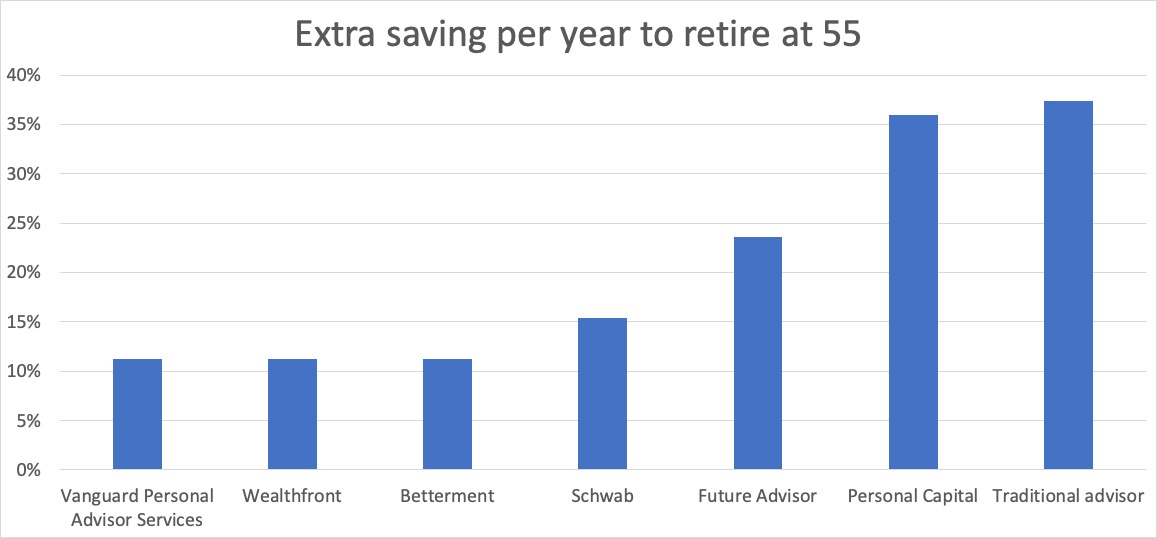

Viewed differently, one can calculate the incremental annual savings rate necessary to neutralize the impact of robo‑advisor fees and preserve the same retirement age as a DIY approach. Our analysis indicates that an investor would need to contribute 11% to 37% more per year to keep pace.

The model assumes that all robo‑advisors achieve market‑matching performance (i.e. the S&P 500) and maintain their fee schedules indefinitely. The latter assumption is relaxed later in the discussion.

Fee components

Robo‑advisors collect compensation in two principal ways:

- A transparent management fee charged as a percentage of assets under management.

- Embedded or “hidden” fees originating from the underlying funds the advisory platform selects. For example, Schwab’s advisory service historically maintained a 6% cash allocation that reduced client returns; this mechanism is a significant revenue source and the focus of recent litigation against the company (see this report).

The table below summarizes the fee structures for the most prominent providers:

| Robo-advisor | Management fee | Hidden fees | Total fees |

|---|---|---|---|

| Vanguard | 0.30% | 0.06% | 0.36% |

| Wealthfront | 0.25% | 0.11% | 0.36% |

| Betterment | 0.25% | 0.11% | 0.36% |

| Schwab | 0% | 0.47% | 0.47% |

| Future Advisor | 0.50% | 0.18% | 0.68% |

| Personal Capital | 0.89% | 0.08% | 0.97% |

| Traditional advisor | 1.00% | 0% | 1.00% |

These fees effectively act as a drag on portfolio returns. For example, a 0.50% management fee reduces a 6% pre‑fee return to 5.50% net of fees.

A self‑directed investor can obtain comparable market exposure at a fraction of the cost. Vanguard’s S&P 500 index fund carries a fee of 0.03%, and competing providers such as Fidelity offer zero‑expense‑ratio index funds (with attention to potential tax consequences in taxable accounts).

Conclusions

For modest account balances, robo‑advisors can still represent an attractive option. Many investors find themselves in a situation where they have exhausted their tax‑advantaged contributions and have incremental funds left; in such cases, the convenience of automation may outweigh the relatively small cost.

However, when dealing with substantial savings intended to fund retirement, the additional fee burden of a robo‑advisor can translate into years of additional work. Regardless of one’s salary, delaying retirement by two to five years merely to pay for convenience warrants careful consideration. The competitive landscape in the robo‑advisor market suggests fees will continue to trend downward, and it may become a compelling choice in the future. As of 2021, though, self‑directed passive investing remains the more cost‑effective option.